AMD Reports Q2 2021 Earnings: Company-wide Growth Drives Doubled Revenue

by Ryan Smith on July 27, 2021 5:25 PM EST- Posted in

- CPUs

- AMD

- GPUs

- Financial Results

- Xilinx

Continuing our Q2 earnings coverage this month, AMD is next out the gate in reporting their earnings. And, has been the story now for most of the last year, AMD is enjoying explosive revenue growth across the company. CPU, GPU, and semi-custom sales are all up, pushing the limits of what AMD can do amidst the current chip crunch, and pushing the company to new levels of profitability in the process.

For the second quarter of 2021, AMD reported $3.85B in revenue, making for yet another massive jump over a year-ago quarter for AMD, when the company made just $1.93B in a then-record quarter. Now, half-way through 2021, AMD’s financial trajectory is all about setting (and beating) records for the company, as evidenced by the 99% leap in year-over-year revenue – falling just millions short of outright doubling their revenue.

AMD’s big run-up in revenue is also reflected in the company’s other metrics; along with that revenue AMD’s net income has grown by 352% year-over-year, now reaching $710M. And if not for an unusual, one-off tax benefit for AMD’s Q4’2020, this would have been AMD’s most profitable quarter ever – and indeed is on a non-GAAP basis. Meanwhile, as you might expect from such high net income figures, AMD’s gross margin has risen even further and now sits at 48%, up 4 percentage points from the year-ago quarter and 2 points from last quarter.

| AMD Q2 2021 Financial Results (GAAP) | |||||||

| Q2'2021 | Q2'2020 | Q1'2021 | Y/Y | Q/Q | |||

| Revenue | $3.85B | $1.93B | $3.45B | +99% | +12% | ||

| Gross Margin | 48% | 44% | 46% | +4pp | +2pp | ||

| Operating Income | $831M | $173M | $662M | +380% | +26% | ||

| Net Income | $710M | $157M | $555M | +352% | +28% | ||

| Earnings Per Share | $0.58 | $0.13 | $0.45 | +346% | +29% | ||

Breaking down AMD’s results by segment, we start with Computing and Graphics, which encompasses their desktop and notebook CPU sales, as well as their GPU sales. That division booked $2.25B in revenue for the quarter, $883M (65%) more than Q2 2020. Accordingly, the segment’s operating income is (once more) up significantly as well, going from $200M a year ago to $526M this year.

As always, AMD doesn’t provide a detailed breakout of information from this segment, but they have provided some selective information on revenue and average selling prices (ASPs). Overall, client CPU sales have remained strong; client CPU ASPs are up on both a quarterly and yearly basis, indicating that AMD has been selling a larger share of high-end (high-margin) parts. According to AMD this is the case for both desktop and laptop sales, and making this the fifth straight quarter of revenue share gains.

Meanwhile the company is reporting similarly good news from their GPU business. As with CPUs, ASPs for AMD’s GPU business as up on both a yearly and quarterly basis. According to the company this is being driven by demand for high-end Radeon 6000 video cards, as well as AMD Instinct (data center) sales. AMD began initial shipments of their first CDNA 2 architecture-based Instinct accelerators in Q2, opening the spigot there for data center GPU revenue going into Q3.

| AMD Q2 2021 Reporting Segments | |||||

| Q2'2021 | Q2'2020 | Q1'2021 | |||

|

Computing and Graphics

|

|||||

| Revenue | $2250M | $1367M | $2100M | ||

| Operating Income | $526M | $200M | $485M | ||

|

Enterprise, Embedded and Semi-Custom

|

|||||

| Revenue | $1600M | $565M | $1345M | ||

| Operating Income | $398M | $33M | $277M | ||

Moving on, AMD’s Enterprise, Embedded, and Semi-Custom segment has once again experienced a quarter of rapid growth, thanks to the success of AMD’s EPYC processors and demand for the 9th generation consoles. This segment of the company booked $1.6B in revenue, $1035M (183%) more than what they pulled in for Q2’20, and 19% ahead of an already impressive Q1’21. The big jump in revenue also means that the segment is even further into the black on an operating income basis, continuing to close the gap with the Computing and Graphics segment even with the all-around growth.

Overall, both the enterprise and semi-custom sides of this segment are up on a yearly basis. AMD set another record for server processor revenue this quarter on the strength of EPYC processor sales. Meanwhile semi-custom revenue was up on both a yearly and a quarterly basis, reflecting the continued demand for the latest generation of consoles.

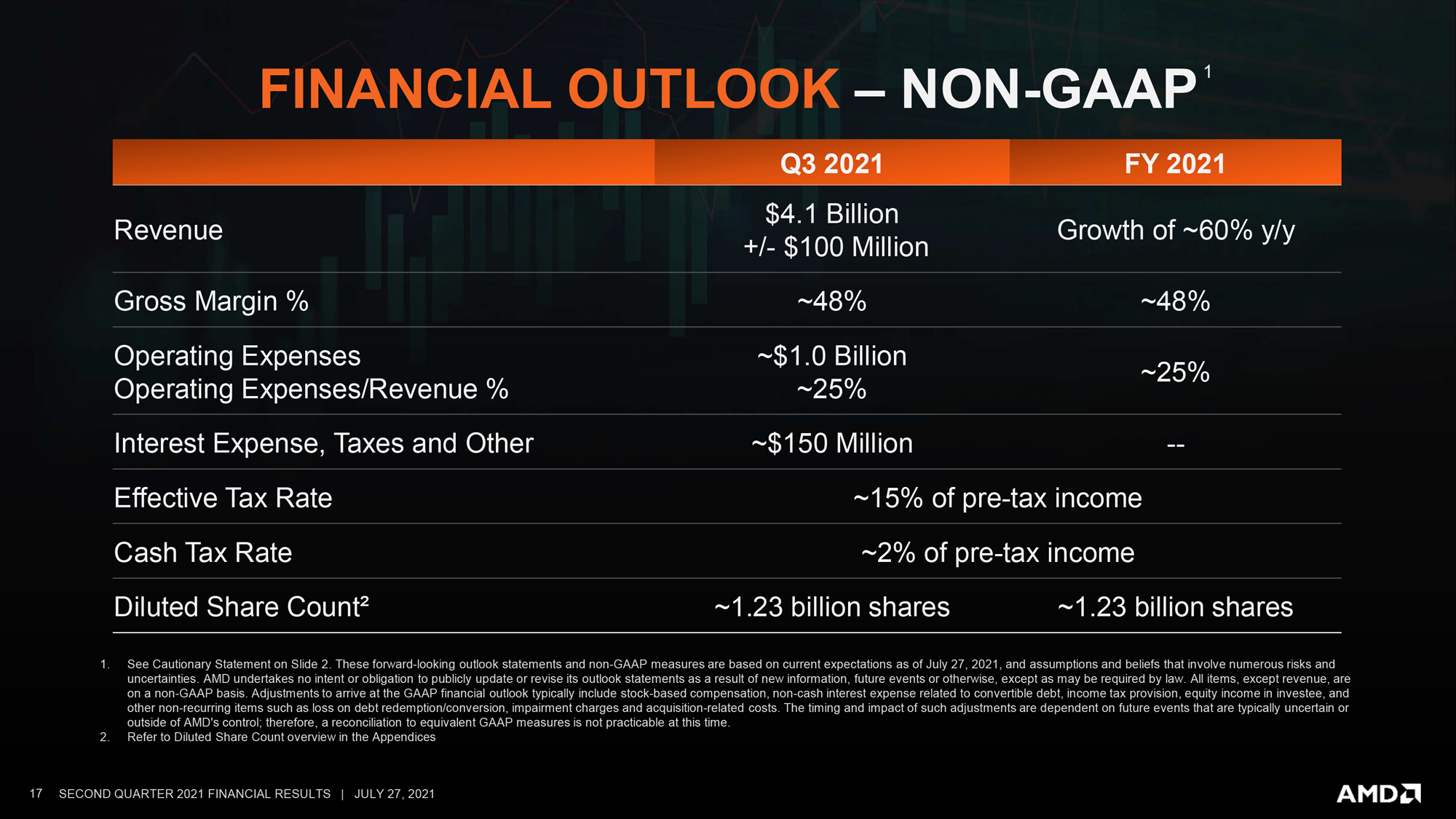

Looking forward, AMD’s expectations for the quarter and for the rest of the year have been bumped up once again. For Q3 the company expects to book $4.1B (+/- $100M) in revenue, which if it comes to pass will be 46% growth over Q3’20. Meanwhile AMD’s full year 2021 projection now stands at a 60% year-over-year increase in revenue versus their $9.8B FY2020, which is 10 percentage points higher than their forecast from the end of Q1.

Finally, while AMD doesn’t have any major updates on the ongoing Xilinx acquisition, the company has reiterated that it remains on-track. Which means that if all goes according to plan, it will close by the end of the year.

Source: AMD

104 Comments

View All Comments

mode_13h - Wednesday, July 28, 2021 - link

Because Apple is more of a lifestyle company than a tech company.All joking aside, Apple is getting big into content, finance, etc. They've outgrown actual technology products, as they search for ways to grow their already enormous revenue.

sseemaku - Tuesday, July 27, 2021 - link

If you look at pc build forums, the results should be obvious. Everyone has Ryzen in their new builds! Still don't understand how Intel lost such a big lead, what were their engineers upto?ikjadoon - Tuesday, July 27, 2021 - link

I was shopping for a new system I wouldn’t want to build anything with Intel today plainly on its heat output alone. Not to mention Intel’s tactics and delays and lies and reheated junk for years.AMD has been killing it and I can only hope they’ll have many more quarters like these so they can really increase their total market share / volume. Intel has been, stubbornly, stuck at 70%+ for two decades. Let’s see a real fight here.

Up to engineering things that clearly weren’t working.

TristanSDX - Tuesday, July 27, 2021 - link

Do you think that AMD is great social company that will make cheapest possible cpu to make folks most beneficial ? Look at numbers again - they are increasing gross margin to level of Intel or more if there will be possibility. When they hit safe ground, then R&D will be decreased, and you will see similar reheated junk, as from Intel.ikjadoon - Wednesday, July 28, 2021 - link

Absolutely not. When that happens, it's time to switch. All companies go through "ah, we need to actually care this time, lol" phases and that's when you buy. Intel can change its tune, Qualcomm, Apple, etc. They all can.Anybody that has "loyalty" to billion/trillion-dollar corporations with millionaire/billionaire CEOs has more than a few screws loose.

Whoever makes the most compelling platform + CPU gets the nod. This isn't too complicated...

mode_13h - Wednesday, July 28, 2021 - link

> When they hit safe ground,I don't think they ever will. Not only will they have a resurgent Intel to contend with, but they'll also have to deal with ARM, RISC-V, the disappearance of the Chinese market, and eventually Chinese competitors reaching markets outside of China.

> then R&D will be decreased, and you will see similar reheated junk, as from Intel.

We don't know that. They don't have the same history as Intel of dividends and share buybacks.

It's possible that, if they plateau at some point, they'll face a lot of pressure from investors to do some of those things in lieu of further share growth. However, that will probably trigger the start of their next big decline.

eva02langley - Wednesday, July 28, 2021 - link

They are debt free and about to acquire the biggest player in the FPGA and microcontroller business.Not only this, but they have a dynamic that Intel cannot match due to their size and agility. Intel is now a conglomerate that can't be stern easily.

mode_13h - Wednesday, July 28, 2021 - link

Yeah and that's great, but they're in a fiercely competitive landscape, right now. They will plateau, at some point. And when they do, it'll be tough to stave off the parasites... er, I mean "investors".eva02langley - Wednesday, July 28, 2021 - link

Two different vision, two different strategy, two different companies.AMD always did it the right way. Claiming that AMD is now going to utilize Intel or Nvidia dirty practices when it is clearly not in their philosophy, is nothing more than you spreading nonsense.

While Nvidia and Intel are bribing studios and AIBs, AMD is releasing open source ecosystem... and from your point of view, these companies are all the same...

LordSojar - Tuesday, July 27, 2021 - link

Being run by MBAs who have no grasp of actual technology. Intel is on a POSSIBLE turnaround now, but it remains to be seen by their execution.